A ring isn't everything

So don't go broke buying one.

Heather here, with the first of several wedding szn posts we’ll be publishing throughout the summer. In the words of revered first-dance singer Chris Martin, let’s take us back to the start with a money-meets-meaning piece on engagement rings.

Been married forever? Don’t worry, they’ll be something for you in this series, too. Also, scroll to the bottom for Doug’s latest reply to people asking their money questions to the open internet.

We’ve been married for almost 13 years, but once upon a delayed engagement ring, I thought I’d be planning an ultimatum instead of a wedding.

I was on my worldwide summer tour telling everyone I’d be getting engaged for my birthday. In my defense, it wasn’t a figment of my imagination. We had discussed it during more than a few “it’s time to take the next step” convos. But when early August rolled around and Doug suggested I pick out a new fall jacket—his treat—I knew something was wrong.

Turns out it was nothing salacious. The jeweler needed more time to recut his late grandmother’s diamond, and poor Doug was feeling the heat. When the ring was finally ready, he pretty much told me point blank to lock in my outfit, get a fresh mani, and meet him for a carefully timed walk home from work that put us right on the steps of Lincoln Center for a golden hour proposal. It wasn’t the most surprising proposal of all time, but looking back, it’s a valuable example of managing expectations. Amirite?!

Summer is prime time for weddings and engagements. Over the next few months, we’ll tap into Wedding Season a bit on The Joint Account. Because even when you’ve moved past being on the circuit every weekend, there’s so much to unpack around family dynamics, expectations between friends, social etiquette, and of course, money, when you’re celebrating a major life milestone for you or someone you care about.

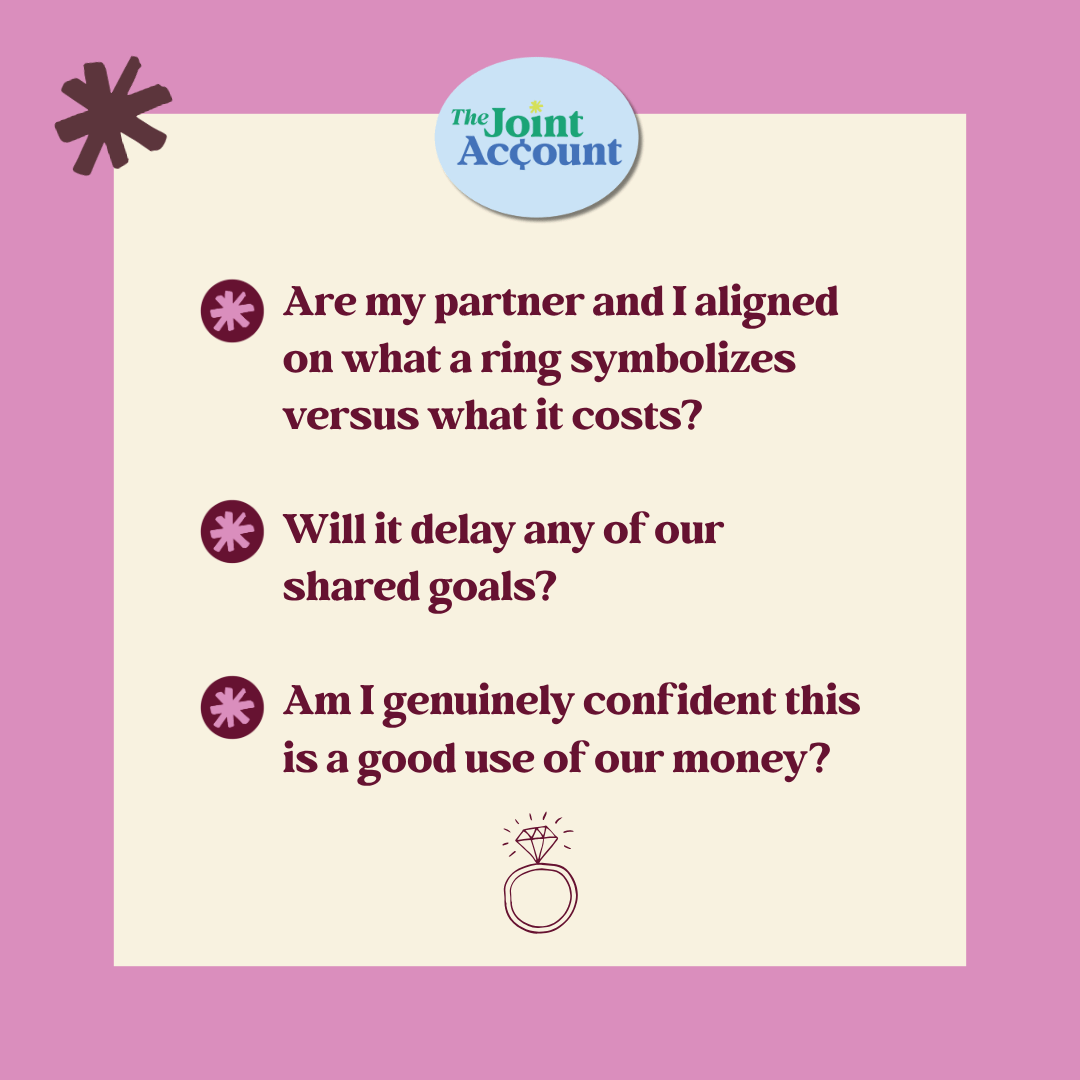

For many couples, buying an engagement ring is the first major financial decision tied to their relationship. It’s a purchase that sets the tone. Whether you and your fiancé-to-be have explicitly discussed a ring budget or not, questions surrounding this grand gesture can easily become a metaphor for everything that follows through the wedding and beyond:

How much do we spend?

Where should the money come from?

Whose expectations are we trying to meet?

So, here’s how to land on a number that makes sense. And if you’re already married, stick with me, because much of our thinking applies to celebrating anniversaries and other life events you may want to spend money on.

First, forget the old rule of thumb on setting a budget. You’ve probably heard some version of “two or three months’ salary,” and we’d encourage you to let that go. It’s not good financial advice. I’m pretty sure some Big Diamond marketing mastermind came up with it.

Today, there are beautiful options at every price point, including lab-grown stones that didn’t exist as a mainstream choice a generation ago. An engagement ring shouldn’t compromise your long-term financial stability or goals, which are much more nuanced than the legacy plug-and-play formula.

To determine how much to spend on a ring, take a look at three things: your cash reserve, your existing debt, and your overall cash flow.

On cash, Doug likes to see individuals and couples work toward having at least six months of their living expenses on hand. A one-time purchase like a ring is exactly the kind of thing you might reasonably dip into your cash reserve for, but you want to be honest about how deep that dip goes, and how long it’ll take for you to replenish your reserve.

On debt, there’s a meaningful difference between carrying student loan debt and high-interest credit card debt. Managing a monthly student loan payment is one thing but carrying a credit card balance that compounds dramatically against you is another, and if that’s your situation, you’ll want to be far more conservative. You would be much better served working to pay down consumer debt before you get married than digging a deeper hole with a larger ring purchase.

Back to the “two-to-three months’ salary” nonsense, income alone doesn’t tell you much about your life without additional context. The real question is how much of your income you’re spending each month and what’s left after that. These are the basics of your cash flow. So, if you’re running a surplus, a portion of that can reasonably go toward a ring budget. If you’re breaking even or dipping into savings every month just to live, you need to ask where your money is going, and whether you need to pare back your spending somewhere to save up a little longer.

People also tend to forget to budget for insurance and upkeep. Expect to pay roughly 1–2 percent of the ring’s value annually in insurance premiums, plus occasional maintenance. Protecting the asset is part of owning it responsibly, and to be honest, if that small added cost is what tips the whole thing over the edge, that’s a pretty clear sign the ring itself is out of your range.

I completely understand how people get in too deep with this purchase. There can be pressure from every angle: your partner, family, friends, the internet. But draining your savings or going into credit card debt to meet someone else’s expectations is a precarious way to begin your financial life with someone else. I get it—trust me, I do—but that doesn’t make it worth it.

If you’re trying to keep the proposal a surprise and can’t exactly sit down to budget this out together, then back into your answer through the conversations you can have about buying a home, paying down existing debt, planning your wedding, and saving for the future. Where a ring ranks among those priorities tells you a lot about the right number. Then, you can ask yourself:

Remember that a ring is just one symbol of your commitment. What actually sets you up for a strong financial life together is communication, transparency, and alignment, the very things this purchase gives you a chance to practice. So do what makes sense for you right now, and don’t let anyone pressure you into a decision that jeopardizes your healthy start.

There will be plenty more to spend on. I promise.

Wedding season is officially underway. What money questions are coming up for you right now? Let us know!

Just married? Your taxes changed more than your last name.

Brought to you by Gelt.

Combining two incomes can quietly push couples into a higher bracket and a bigger bill, especially for business owners and high earners. Gelt pairs you with a dedicated tax advisor and smart technology that plans year-round, so you and your partner stop overpaying and keep more of what you built together. See what proactive tax strategy looks like at joingelt.com. #sponsored

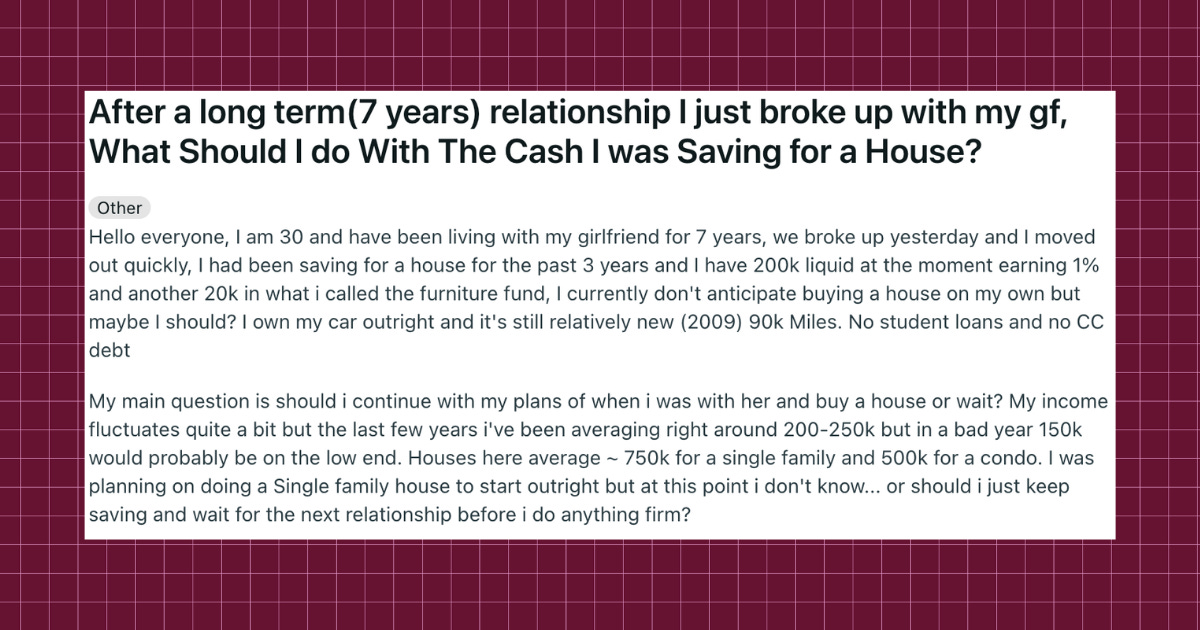

The breakup doesn’t change the math, but it does remove the deadline.

I think the worst move this guy can make right now is forcing a decision while he’s still dealing with moving out. And the real problem isn’t whether to buy…it’s the $220k sitting in cash earning 1% while inflation eats him alive.

The good news is that it’s a fixable mistake regardless of what he does about a house. He needs to park it somewhere boring and liquid like a high-yield savings account or in short-term Treasuries (earning 3 to 4 percent as of today) and give himself permission to do nothing for six months. He should also stop tying a house to a relationship that doesn’t exist yet, because you buy a home when you want a home and can afford one, not because a future partner might show up someday to help fill it. -Douglas

Want to go deeper? Money Together is everything we’ve learned about love and money, told through real stories with lessons for couples who want to build a financial life together without losing themselves in the process. Order your copy on: Amazon, Barnes & Noble, Bookshop, or Audible (narrated by Heather!).

Love it already? A review on Goodreads and wherever you purchased helps other couples find us and means more than you know.

Bring us to your organization! We speak on money, relationships, and what it really takes to build a financial partnership that lasts. Available for corporate events, conferences, and private engagements — virtually and IRL. Reach us here.

Connect with us on social: @averagejoelle + @dougboneparth

The content shared in The Joint Account does not constitute financial, legal, or any other professional advice. Readers should consult with their respective professionals for specific advice tailored to their situation. The information contained in this post is general in nature and for informational purposes only. It should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This post is not a solicitation or an offer to buy or sell any specific security. Bone Fide Wealth cannot guarantee the accuracy of information from third parties.