How to raise kids who are good with money

Financial literacy starts earlier than you think. Here's what to teach them at every age.

When Ruby was three or four, one of her little-kid things broke. I don’t remember what it was, because what she said after struck me to my core.

She said, “It’s okay, Mama. Amazon Prime can bring us another one tomorrow.”

I’m sure some of you think this was an adorable thing for her to say. But given what we do for a living, coupled with my millennial agita to raise good humans, I felt a sense of existential dread over what our girls were learning from us.

April is Financial Literacy Month for adults and kids alike. The moment our children are old enough to observe our behaviors, they are picking up messages that form the foundation of their beliefs about money. I know this, because I spent nearly two years asking people about their earliest memories of money for our book. You didn’t have to stretch to see the throughlines between their childhood and what they believe now. Almost everyone had something to say about when they were young.

As parents, we are part of their origin story—for better or worse.

Before I got into this work, I had a very limiting view of what it meant to become “literate” with money. I thought it just meant learning basic financial concepts like budgeting, understanding your cash flow…the kind of things you should be learning in a foundational classroom setting. According to Next Gen Personal Finance, 30 states now require coursework in financial concepts to finish high school, which is awesome. But I would caution any parent of young children against kicking this can down the road until then.

We can help our kids establish strong foundational beliefs long before they can grasp advanced math concepts. We can help them create good habits, build confidence, and learn how to be critical about decisions that impact their futures. You don’t need a lesson plan for this work. It’s rooted in how we’re speaking to our kids at Target, and how we talk to each other around the dinner table. It’s holding the line when giving in feels easier, and creating friction in a world designed to make spending as easy as possible.

Douglas and I have written about money and parenting before (like, many times before). But in honor of Financial Literacy Month, I want to offer you some big-picture ways to think about leveling up your kids’ understanding of money from a young age through early adulthood.

If they’re old enough to speak, you’re old enough to start.

Let me show you.

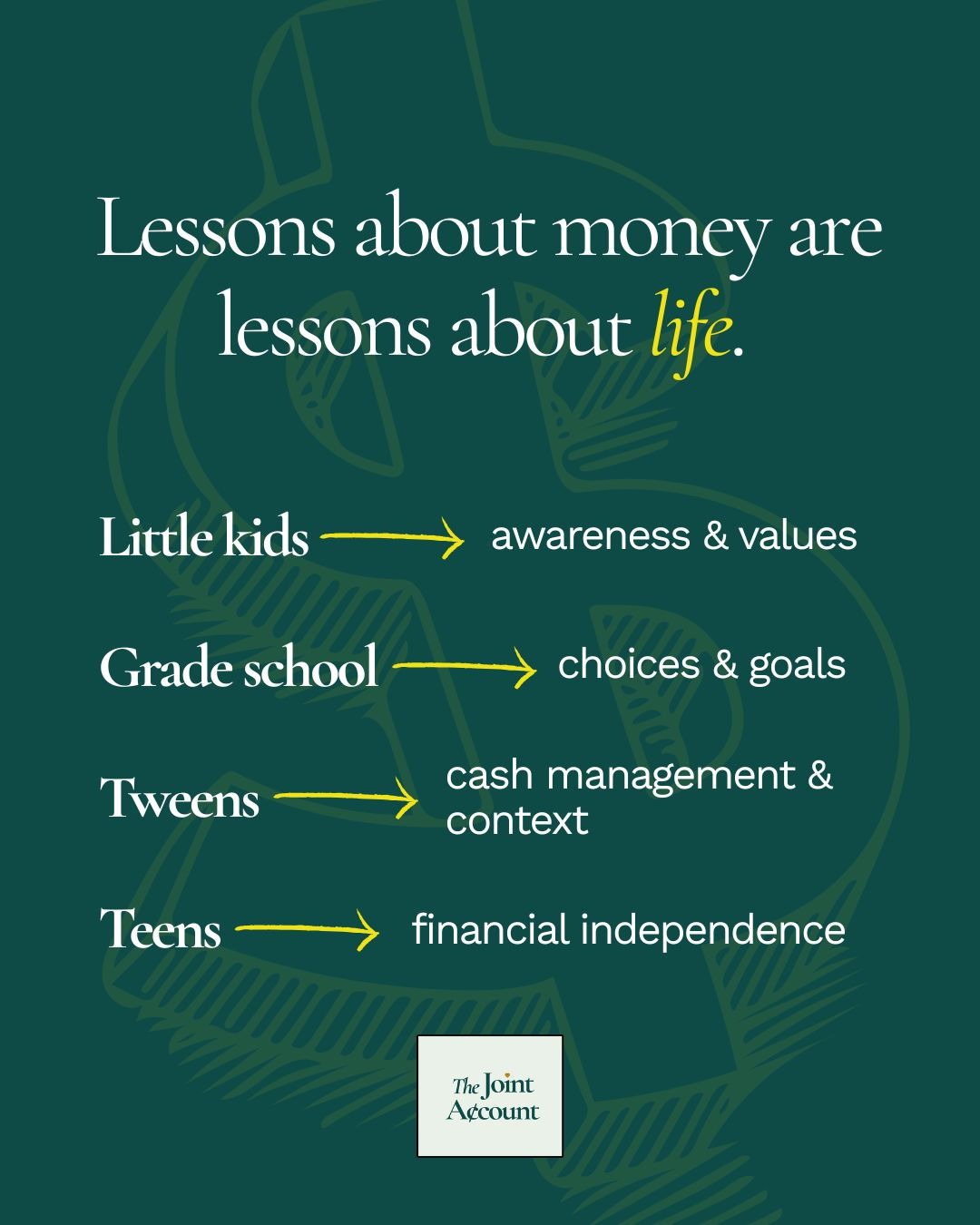

Little kids

When it comes to your kids’ earliest understanding of money, focus on instilling values. The financials and vocabulary will come later. You want to show them through simple, real-world examples that we make choices every day, and we put careful thought into what they are.

Life is not one big trip to the all-inclusive Amazon Prime resort.[1] Three-year-old Ruby once believed it was, but she now knows that things do not just “appear.” We choose to buy them, either because we need them or because we want them and have decided it’s an appropriate time to purchase. Waiting is normal. You can get your kids comfortable with the fact that you’re making decisions based on what something costs, even before they have the context for what “expensive” means.

The grocery store is a great place to practice. I used to read Ruby the prices of produce, like avocados or apples. Then, I’d have her physically hand them to me while counting. Once we got close to how many we needed, I’d ask her, “Do you think we need another? Do we need five or is four enough?” I’d suggest to her that if we got three, we could get strawberries, too. We were making choices around spending in a way that didn’t make money feel threatening or scarce.

One of the earliest connections we drew for our girls was between money and work. When I was a mega-commuter, Douglas would drop me off at the train station before taking Hazel to preschool. She asked him why they always had to do that. He’d explain to her that the reason we got to enjoy many of the things she really likes—Presents! Disney World! Trips to the ice cream place!—is because we earn money that pays for these things at our jobs. And even though Mom would much rather be driving you to preschool, she has to take the train to work.

In other words, we earn money by working, even when it’s not the most fun thing to do, and then we use that money to live and enjoy our lives. It’s not a hard concept for them to grasp but an important one.

One more point on values: having kids is a great time to revisit yours.

Giving is very important to me, but to be honest, it wasn’t a priority in the early and expensive years of our careers in New York City. Once the girls’ preschool introduced the concept of tzedakah (charity) to them, I knew it was time to find new ways to begin to embody the generosity that always lived in my heart. So, we volunteer. We donate money. We’ve held board seats and pro bono positions for non-profit organizations. Many of the activities centered around our values involve our kids, so they really do begin to form not only the connections between what you believe and what you choose to do about it, but they start to gain context. More on that later.

Grade school

By the time kids arrive to grade school, they’re starting to learn basic math. They can listen and comprehend more complex ideas. They’re also expected to begin taking some personal responsibility for themselves. But what’s hard about this phase is that kids don’t really grow in a straight line. Recently, a friend said to me that she feels like one day she’s parenting a teenager, and the next, she’s parenting a little boy. I’m right there with her.

As our kids mature, certain concepts might kind of make sense to them, but that doesn’t mean they’re emotionally or developmentally ready to execute on them all the time. So, don’t be discouraged if you read this and think, there’s no way we’re ready for that. All good.

We’re also putting allowances aside for today, because the question of whether your kids should have them (and if so, how much) is complicated. My close friends tie the money they give their kids to expectations around personal responsibility rather than a list of chores, which I really like. But because this topic requires a longer discussion, let’s just hold true the fact that our kids may start to acquire money around this time, whether it’s from an allowance, the tooth fairy, birthday presents, or their grandparents giving them a dollar for no apparent reason.

The core lessons at this phase are still about choices, but they’re much more meaningful to them than a trip to the grocery store. There are things with price tags that school-aged kids really want.

This is the time to show them how to:

earn,

save, and

spend money with purpose.

They can learn about prioritizing when there’s several things they’d really like to have or do. And they can begin to understand real value—what’s worth it and what’s not.

Elementary school is a great time to encourage your kids to save for their first financial goal. Hazel, for example, really wanted an iPad that wasn’t whatever first-generation brick she inherited from us. At the start of the year, we showed her how much it cost, and we counted how much money she had. We discussed her paths to get there and offered for her birthday to match whatever dollars she could save that year. When it came time for her to hand over her roll of cash to us, she was proud, and we were impressed. She really had her eyes on the prize.

Budgeting can also become a powerful tool. For special outings to the toy store or Sephora (eek), I like to set budgets and give them the freedom to make decisions for themselves. Sometimes, they have to make hard choices, but they’re less upset when it’s their choice to make. My only caveat to an exercise like this is to be careful you’re not imparting fear or stress on your kids by telling them they only have X, because we can’t afford more. Parentifying your children by infusing your money worries into their special moments is something they’ll remember for a long time. Again, I’ve seen some things. Just do your best to avoid it.

Tweens

Welcome to tweenhood, a brief pitstop when everyone’s growing, smelling, yelling, and crying.

I kid, but there’s a whole lot of truth to how challenging these couple of years can be. Between the hormones and the added sense of self-awareness, tweens have a lot to be emotional about. Small things feel like big things. Minor problems feel like the world is ending. Without belittling their very real feelings, this may be the perfect time to introduce some more context into their lives.

I think most young people tend to fixate on what they don’t have before they consider what they do have. It comes with the territory. Some of the people we interviewed said that their earliest money memories came by comparison—by realizing they have less than someone else. It’s okay to acknowledge how frustrating that might feel and not gaslight them into believing we all just operate in our own financial silos, immune to the weight of how unfair the world is.

Privilege shows up in visible and invisible ways. You can, and should, begin to talk about it. Your tweens are old enough to hold two truths: they can wish something was different, and they can be grateful for what they have. But they’ll need your example to begin to see it that way.

In terms of hard dollars, this could be a great time to advance the concept of budgeting into the early stages of cash management. As they socialize and spend more independently, consider letting them manage a small monthly budget for things you used to just give them, like clothes or after-school snacks in town. You’re obviously not going to hand the reins over to them entirely, but you’ll all learn a lot from giving them a bit more agency.

I would also consider opening a debit card for them, not only to simulate how money realistically changes hands in the real world but to give them visibility into banking systems. There are so many cash management tools out there to help them begin to understand their spending habits even at this stage. Don’t sleep on the chance to start them out before you really need to.

Teens and young adults

This is the main event. It’s where you pair the values, attitudes, and behaviors you’ve been working on with hands-on lessons from the real world so your kids can become independent and financially literate members of society. No pressure, though!

Bearing in mind how long this manifesto already is, I will touch on all the important concepts but keep it high level. This is work to be done over years; not months, and certainly not in one sitting from reading our newsletter.

Taxes, withholdings, and how money flows

Part-time employment during high school or college is the perfect time for teens and young adults to familiarize themselves with how paychecks work, and how money flows in and out of their financial lives.

How much you make is not how much you take home. Teach them how to read their pay stub and learn the difference between gross and net pay. Have them see how much money is withheld for taxes and other types of deductions. They need to learn that the take-home amount is how much they are left to work with, and only then can they begin to understand what they truly can and cannot afford.

On cost of living, most young adults can easily find out how much rent would cost in a place they want to live, but rent is just the first expense. Utilities, internet, and transportation costs are musts. Then, there’s the more invisible costs, like insurance (including maybe renter’s insurance), deductibles to even use that insurance, and memberships and subscriptions that feel critical to their lifestyles but really add up. This is not including food and groceries, which will eat up more of their “adult” paychecks than they probably realize.

You may not be able to simulate the true feeling of “leaving the nest” for them. They may just need to see for themselves. But if you need to start showing them what your life as a family costs to make this all seem realer to them, don’t shy away from it.

Credit and consumer debt

While credit itself is not a complex topic, teaching teens the correct way to use it might be. On one hand, you want to build credit as a young adult—your credit score can make or break your ability to rent an apartment, buy a car, or even start a business down the road. You build credit by using credit and then paying off your monthly amounts owed in a timely fashion. I’ll never forget my first American Express Blue for Students card. In fact, I still have it!

Unfortunately, Buy Now Pay Later options are being marketed directly to young adults to finance everything from groceries to clothing. It’s a dangerous game to believe you can make minimum payments on a burrito, because financing small expenses is a slippery slope into losing control over your consumer debt and destroying your credit. While you can, teach your kids that these are not viable options for financing your lifestyle.

Investing and building wealth

Investing early can give young adults an enormous head start, but our concept of what it means to invest is likely not the same as theirs. Young adults are being taught via social media and tech-forward investment platforms that investing is more like gambling—that it’s a risky, short-term game with winners and losers. For most, the gamification of investing works against building long-term wealth.

Teens should be learning about compound interest, appreciating assets, employer matches, and setting automatic transfers into investment accounts. They should be learning about having their money work for them through patience and discipline, not doing “the most” work while risking too much.

ROI (return on investment) in higher education…and everything else

It’s true that higher education is an investment in yourself, but how do you measure the return on that investment? You would think that because so many millennials are still saddled in student loan debt, higher education would be dramatically different by now. But striving culture still exists. Encourage your teens not to chase clout but to critically understand whether the career they want warrants the cost of the degree.

Teens need to learn about interest and how it compounds on top of principal amounts borrowed. They need to learn the difference between federal subsidized, unsubsidized, and private loans. And in my opinion, they need to understand just how opaque and impossible it is to deal with student loan servicers after they graduate. There is virtually no safety net in that system, and they will need to know how to advocate for themselves to get anything done.

You can show them how this concept will continue to apply throughout their lives. When you invest in something—whether it’s your own advanced degree, an idea, a publicly traded company, or even another person—you should be doing your own research to determine whether you believe you’ll get what you want out of it. Things don’t always work out, of course, but due diligence lessens the chances of making ill-informed choices they’ll come to regret.

Lessons about money are lessons about life. The conversations you have now will compound over time, shaping how your kids think, feel, and act long after they leave home. Let Financial Literacy Month be your starting point, because the way we talk about money today becomes the voice our kids hear in their heads tomorrow.

Parents, let’s support each other. What’s worked for your kids? What hasn’t?

Comment below or reach us here.

TJA’s Couple of the Week

Speaking of Mother and Father, my Couple of the Week goes to the Biebers, the prom king and queen of Coachella this past weekend. JB set the internet ablaze with his headline set that gave us the classics, while Hailey turned the desert into a Rhode playground with brand activations that flooded my social feeds. They even had Kylie acting basic—an outstanding circus to obsess over from my Couchella. -Heather

Friendly reminder to our free subscribers: all new posts arrive in your inbox. After 14 days, they will be placed behind a paywall on our site. If you love The Joint Account and want complete access to our archives, a monthly AMA with us, bonus video content, and more, please consider becoming a paid subscriber.

Money Together is here. If you find value in our newsletter and want to support our work, please order a copy today: Amazon, Barnes & Noble, Bookshop, or Audible (narrated by Heather!).

Love it already? PLEASE, PRETTY PLEASE leave us a review on Goodreads and wherever you purchased.

Want more Heather and Doug? Have us come talk about love and money with your organization—virtually or IRL. Reach us here.

Connect with us on social: @averagejoelle + @dougboneparth

The content shared in The Joint Account does not constitute financial, legal, or any other professional advice. Readers should consult with their respective professionals for specific advice tailored to their situation. The information contained in this post is general in nature and for informational purposes only. It should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This post is not a solicitation or an offer to buy or sell any specific security. Bone Fide Wealth cannot guarantee the accuracy of information from third parties.

[1] BTW, we just went to an all-inclusive resort with the girls, and I was very proud to hear Hazel correct Ruby after she said, “Everything here is free.” Hazel told her, “Everything here is not free. Mom and Dad paid for it before we came.” We love to see it!

Great advice and lots of things to think about! I wanted to share another perspective on the elementary schooler advice to avoid the phrase "we can't afford it." I actually copied and pasted this quote from an old magazine of my Dad's because it really resonated with me:

"Four magic words, 'we can’t afford it,' should be a part of every child’s education. A child who has never heard those words – or also has never been forced to abide by their meaning – has surely been cheated by his parents. As exercise strengthens the body, frugality strengthens the spirit. Without its occasional discipline, character suffers.”

As a family who generally has the money for needs and wants, I think it's actually really important for my kids to hear "we can't afford it" - or, at least, "that's not how we're choosing to spend our money right now." Of course we don't want to transfer money stress to our kids, but I think we can help them understand that life has trade-offs. I definitely heard this from my parents growing up, and I think it really benefitted me. Just offering another perspective!

I’ve seen this from both sides as someone who inherited odd money patterns and as a coach helping people untangle the ones they’re passing on without realizing it. Just wrote about this same topic. It matters more than people think.