Don't start a GoFundMe for your medical bills just yet

How to reduce costs, exhaust resources, and make people do their jobs.

Over the past few weeks, you may have seen the debate surrounding the late James Van Der Beek’s GoFundMe campaign, which at the time of this publication, raised more than $2.7M. Regardless of how you feel about a famous family or the politics of healthcare, you can’t ignore how the untenable economics of medical costs in the United States are playing out for real people every day. According to a study from the American Cancer Society, roughly one-third of all GoFundMe campaigns seek help paying for medical expenses. One-third.

If you ask me, we’re long past the time to wag our fingers at anyone and cite personal responsibility for a system that leaves so much room to destroy lives. People end up exposed in any number of scenarios. Imagine you receive a diagnosis while you’re between jobs and can’t afford the full cost of premiums under COBRA to keep your decent insurance coverage. Or your partner’s been hospitalized, and even though you’ve got an out-of-pocket maximum, you don’t have $9,000 in cash to spare.

In this season of The Pitt, a father suffering from diabetic ketoacidosis revealed he was insulin rationing, because he couldn’t afford his prescribed dose. Instead of accepting help from a GoFundMe campaign that his daughter started to support his hospital stay, he was ready to walk out and risk his life, in a classic illustration of how money is more than money. Even just the emotional impact of accepting help can bear down on you long after your medical needs are met.

I could outline a hundred more examples, and I’m sure you could offer them, too. This is more than an isolated problem—it’s a moral failure that highlights a gaping hole in our societal infrastructure. What a beautiful thing to financially have your neighbor’s back. But what a disgrace that we need to.

On The Joint Account, I’ve covered many angles of healthcare and insurance, but what I’m sharing here today is for everyone.

Before you turn to crowdfunding for your medical expenses, you deserve to understand—and exhaust—the resources designed to carry this burden in the first place. Hospitals, insurers, government agencies, and even targeted non-profit organizations have the scale and capital to absorb the appropriate costs of your care. You need to know how to make them. These are the steps to take first.

Let your community carry you through meals, childcare, love, and support. Not the full costs of bills dropped on your shoulders.

Steps to take before crowdfunding your medical bills

Ask questions before testing or treatment

Under the No Surprises Act, if you don’t have (or don’t plan to use) health insurance to pay for your care, you have the right to request a good faith estimate for medical services. You just need to make the request at least 3 days in advance. You may be able to contest your bill if the difference is greater than $400.

Even if you do plan on submitting a claim to your health insurance, asking for more information helps you identify where the sticking points might be. I’ve previously shared the recurring issues I’ve had with billing for breast cancer surveillance. By raising past coding issues and discussing the potential for uncovered services beforehand, you might be able to lock in a price for services that’s lower than whatever the bill looks like after it’s been passed through several departments of a major medical conglomerate.

You may not be able to get every answer you’re looking for, and remember that estimates (as with any service) have a right to change. But asking for them is very important. It holds people to a standard deviation. It creates a record. It’s the beginning of a story you might need to tell later.

Request itemized bills

Have you ever logged into a patient portal and seen the words “YOU OWE” with almost no explanation offered? That’s unacceptable. Don’t settle for whatever appears on a portal dashboard or the cover page of an invoice. Request an itemized bill, because you never know what you’ll find.

Some things to look for include:

Duplicate charges

Incorrect services that weren’t even rendered

Inapplicable fees

Incorrect billing codes

Out-of-network charges at in-network facilities

Note that some of what you’ll find on an itemized bill may not be right or wrong. As was the case with my annual mammogram, some services can be billed under multiple codes with different outcomes. And some out-of-network services exist at in-network facilities, but the patient should be asked to consent to those services beforehand or not be charged the uncovered balance for them.

At this stage, your goal is to learn as much as you can about the story of the costs you’re being asked to pay. You can even compare your costs to industry standards using resources like FAIR Health Consumer. You’ll need these details to appeal and negotiate.

Appeal, appeal, appeal

If you’re unhappy with your health insurer’s handling of your claim, appeal. Appeal like you’ve got nothing to lose, because you don’t.

Begin with an internal appeal through your health insurer. And lean on your doctor for support: request they submit your claim under a different code or prepare a letter of medical necessity. Be courteous but specific and direct in what you’re asking for.

I wouldn’t give up after one shot—try twice.

If your insurer upholds its denial, you have the right to file an external appeal. This would place your claim before an independent panel of medical professionals, and their decision would be binding on your insurer. The procedures vary by state, so be mindful of deadlines.

Negotiate the remaining amount

Here’s a lesson much bigger than bills: ask for the things you want. In a study from the USC Schaeffer Center, 76 percent of respondents who reached out regarding an unaffordable medical bill were offered some form of financial relief. Out of those who negotiated, 62 percent said their price was lowered.

When you do reach out to the billing department, find out your options. Ask what happens if you paid the bill in full today. Many providers are willing to negotiate a significant prompt-pay discount. If that’s not an option for you, ask about a no-interest payment plan. Yes, you read that right: zero percent, which means you can spread the payment out over months and ease your burden without owing more. Also, discuss whether you qualify for financial assistance and charity programs that might be available.

I know it’s scary to have a big outstanding bill, but please don’t charge it to a credit card because you’re afraid. As of 2023, the three major consumer credit reporting agencies stopped including medical collection accounts under $500 on credit reports. In 2025, the Consumer Financial Protection Bureau was set to enact a rule removing all medical debt from credit reports, but you can bet who put that rule on ice. Some states still offer protection, but what’s important for everyone to know is that medical debt likely won’t appear on your credit report until 365 days after your payment is delinquent.

In other words, you have time: time to regroup, time to negotiate, time to set a budget, and time for a plan. But you won’t have that leniency if you put it all on a high-interest credit card. Then, it’ll just be another bill.

Ask a professional for help

You don’t have to sort this out on your own. Many states offer consumer assistance programs. Here’s a map to look for yours.

A nonprofit called Dollar For helps individuals apply for medical debt relief from hospitals. You can find out if you qualify for their assistance.

And if you’re just too overwhelmed by medical jargon, a complex bill, or the continuing stress of an ongoing illness, consider hiring a medical billing advocate. Just be sure to do your own research to find the right person and understand how this person gets paid. Some have hourly rates and others operate on contingency; meaning, they take a percentage of the money they are saving you.

Exhaust all prescription discount options

If you’re being prescribed a medication that isn’t covered by insurance or comes at too high a cost, you’ve got options here, too. Start with your medical provider and your pharmacist, because they’re probably the most familiar with the avenues you can take for the drug prescribed.

You want to ask about:

Discount cards and coupons

Manufacturer assistance programs

Generic alternatives

Price breaks on 90-day refills versus 30-day

Using a mail-order pharmacy

When I was pregnant with our second daughter, our health insurer tried to tell me that my weekly progesterone shots to prevent pre-term labor were only available in their preferred manufacturer’s new auto-injector, which even with insurance, would still cost more than $4,000 per month. (My mom took progesterone shots in 1985, so it wasn’t the meds—it was the injector.) Though it took a few wrong turns, a scathing email, and one emotional plea to the manufacturer assistance program’s patient advocate, they ended up asking how much I could afford to pay. I said almost nothing, and that’s what they basically charged me. Don’t give up.

Search for grants and foundations

In the same sense that smaller scholarship programs can end up underutilized, consider that there may be a whole host of organizations with resources to help people in your position. They can offer financial assistance, travel grants, lodging support, and even childcare support.

Look to state and local programs, disease-specific foundations, religious-based grants and assistance programs, veteran’s programs, employee hardship funds, and even programs run by industry associations you belong to. There could be more help available than you realize.

If you’re going through something that makes this far too relevant, I’m sorry.

But before you click “start fundraiser” in a panic, take a breath and work this list. Screenshot it, share it with your partner or support network, divide and conquer. If you know someone who needs help, forward this to them. We can carry each other in many ways, but we don’t need to stand on the front lines.

Have you managed an unexpected medical bill? Let us know.

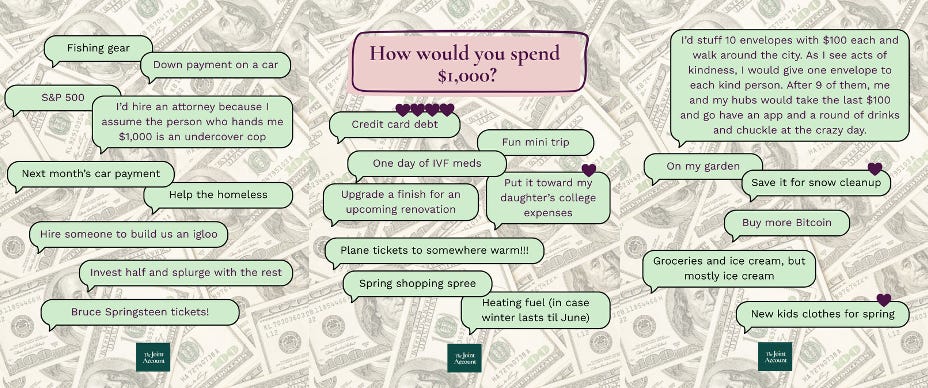

HWYS $1,000?

Welcome back to our mini-series, How Would You Spend? This time, we’ve upped the ante to $1,000, an amount that proved meaningful to many but still left the door open for impulse spending. Notice the “weather-related skew” - maybe we shouldn’t have asked during a massive blizzard! Anyway, here’s how you’d spend it:

Money Together is here! Order now in your format of choice.

Love it already? Leave us a review wherever you purchased!

Want more Heather and Doug? Have us come talk love and money at your organization—virtually or IRL. Reach us here.

Connect with us on social: @averagejoelle + @dougboneparth

The content shared in The Joint Account does not constitute financial, legal, or any other professional advice. Readers should consult with their respective professionals for specific advice tailored to their situation. The information contained in this post is general in nature and for informational purposes only. It should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This post is not a solicitation or an offer to buy or sell any specific security. Bone Fide Wealth cannot guarantee the accuracy of information from third parties.